In this edition of Critical Thinking, Peter Hütte considers how Africa’s critical minerals supply routes are being reshaped amid intensifying US–China competition for strategic resources.

Two railway projects in Africa—one heading west across southern Africa to the Atlantic and another, in the east, heading to the Indian Ocean—have emerged as the defining infrastructure contest in the continent’s critical minerals landscape. Both projects are decades old, but in the past two years they have become extensions of a heated competition between China and the US to secure mineral supply chains.

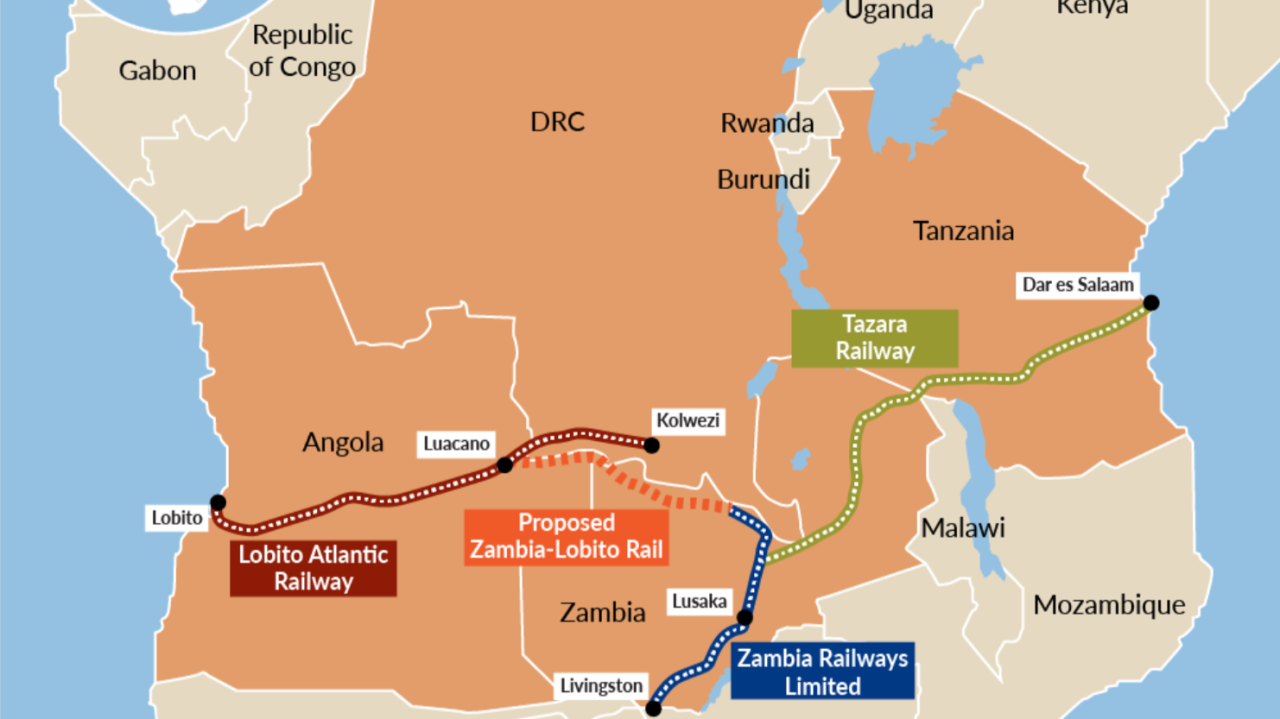

The Lobito Corridor

The Lobito Corridor is a multimodal transport network linking Angola’s Atlantic port of Lobito to the copper and cobalt producing regions of the DRC and Zambia’s Copperbelt. Its backbone, the Benguela Railway, dates to the early 1900s and was rehabilitated between 2004 and 2014 under a US$2 billion Chinese rail-for-oil program.

The G7-backed Western phase began in earnest in 2022, when a private consortium—the Lobito Atlantic Railway, which comprises Trafigura, Mota-Engil, and Vecturis—took a concession to operate and upgrade the line. Combined US and EU support now exceeds US$4 billion, anchored by a US$553 million DFC loan finalized in December 2025 and approximately US$600 million in separate US commitments for expansion into Zambia.

The corridor is partially operational. The Angolan section facilitates regular shipments of copper from the DRC and monthly sulfur imports to support Copperbelt mining operations. The DRC section remains severely degraded, operating at a fraction of its design capacity, and ground is yet to be broken for the Zambia extension. With an annual cargo of 230,000 tons and a target of 1 million tons by 2030, the project’s strategy lies not only in what it moves but where: westward, toward Atlantic markets, and away from Chinese-controlled export routes that currently dominate Copperbelt mineral flows.

TAZARA

China’s response to the Lobito Corridor has been direct. In November 2025, Beijing signed a US$1.4 billion, 30-year concession agreement with Zambia and Tanzania to rehabilitate the TAZARA railway, a 1,860-kilometer line running east, linking landlocked Zambia to the Indian Ocean port of Dar es Salaam, where the UAE’s DP World manages two-thirds of port operations under a 30-year concession signed in 2023.

The deal is part of China’s Belt and Road Initiative and widely understood as a deliberate counter to Lobito. China’s approach to African infrastructure financing has grown more selective—large-scale lending has given way to stricter project review and a clearer expectation of economic returns, whether through resource access, repayment capacity, or transport leverage. Strategic corridors that meet this bar, like TAZARA, continue to attract full state backing.

Under the concession, Chinese firm CCECC will finance, rehabilitate, and operate the line while Tanzania and Zambia retain ownership. Tanzania sees the corridor as central to its ambition to become East Africa’s dominant trade hub, giving China additional incentive to keep Dar es Salaam within its orbit. The strategic logic mirrors Lobito’s, but in reverse: route minerals eastward, toward Chinese-controlled processing facilities and markets.

Different Models, Different Timelines

The two projects reflect meaningfully different approaches. Lobito is structured as a public-private partnership with open-access rules, backed by multilateral development finance and private capital alongside US government support. Its governance model is complex and its execution timelines long, encumbered by multi-party coordination and significant financing gaps in the DRC and Zambia segments.

TAZARA, by contrast, benefits from a single state-backed funder with a 30-year operating commitment. China’s model bundles financing, construction, and operations under one roof, reducing coordination costs but embedding long-term dependence. The tradeoff is a familiar one across Chinese infrastructure investments in Africa: Delivery is faster and conditions are fewer, but terms tend to favor Beijing’s strategic interests over time.

What This Means for African Countries

The contest has given DRC, Zambia, and Tanzania agency, and the governments of all three are using it. Each is pursuing a pragmatic policy of competitive multi-alignment, welcoming both Western and Chinese investment while using interest from one side to extract better terms from the other on local processing, revenue sharing, and labor standards.

Zambia last year became the first African country to officially accept China’s yuan for mining royalties while simultaneously committing to a plan with Washington aimed at unlocking a substantial grant package in exchange for mining-sector collaboration and business environment reforms.

Tanzania is in discussions with the US on flagship investments in nickel and graphite, specifically the Tembo Nickel Project and the Mahenge Graphite Project, while continuing to host a dense layer of Chinese medium-scale operators and maintaining the TAZARA concession.

The DRC has granted US companies preferential access to mining licenses under the US-DRC Strategic Partnership Agreement, while Chinese operators press ahead—CMOC announced major capital commitments last year to its Kisanfu and Tenke Fungurume copper-cobalt mines.

The leverage runs both ways. Washington has used the prospect of the Zambia extension to press Lusaka on mining-sector reforms, while Beijing’s infrastructure commitments carry their own expectations. The room for maneuver has limits too. China’s dominance in downstream processing means that even where Western companies hold mining licenses, minerals often end up flowing through Chinese refineries, and whoever moves the ore tends to influence where it goes.

The next test will be operational. Lobito needs to close financing gaps in the DRC and Zambia segments and demonstrate that its open-access model can attract enough volume to be commercially viable. TAZARA needs to prove it can handle bulk mineral freight after decades of underinvestment. Until both are running at scale, African governments will continue to keep their options open.

What This Means for Operators

For mining companies operating in the region, the corridor contest is a commercial variable, not just a geopolitical backdrop. Which route a company uses, which financing partners it works with, and how its ownership structure is perceived in Washington or Beijing will increasingly affect access to capital, offtake agreements, and government support.

The timeline, however, is long. TAZARA’s rehabilitation is projected to take around three years; Lobito’s critical segments in the DRC and Zambia have no firm construction schedule. The flagship mining projects currently being negotiated across all three countries will take years to reach production.

Companies that map this landscape now—which routes serve which markets, how host government policies on processing and local content are evolving, and where US and Chinese financing is likely to flow—will be well-positioned when the pieces finally come together.